Insurance Rates Are Cooling in 2026. Here's Why You Still Need an Independent Insurance Agent in Utah

By Jett Iverson, Director of Marketing | The Insurance Center

Published: July 2026 | Farr West, UT serving Northern Utah and beyond

Your renewal notice showed up, and the number went up again. Maybe not as much as last year, but it went up. If you've been hearing that the insurance market is finally stabilizing in 2026, that headline probably didn't match what you saw on your own bill. Here's the short answer: market-wide stabilization doesn't mean every carrier treats you the same way, and the only way to know if you're actually getting a fair deal is to have someone shop it for you. That's what an independent insurance agent in Utah does that a single carrier's website or a captive agent never will.

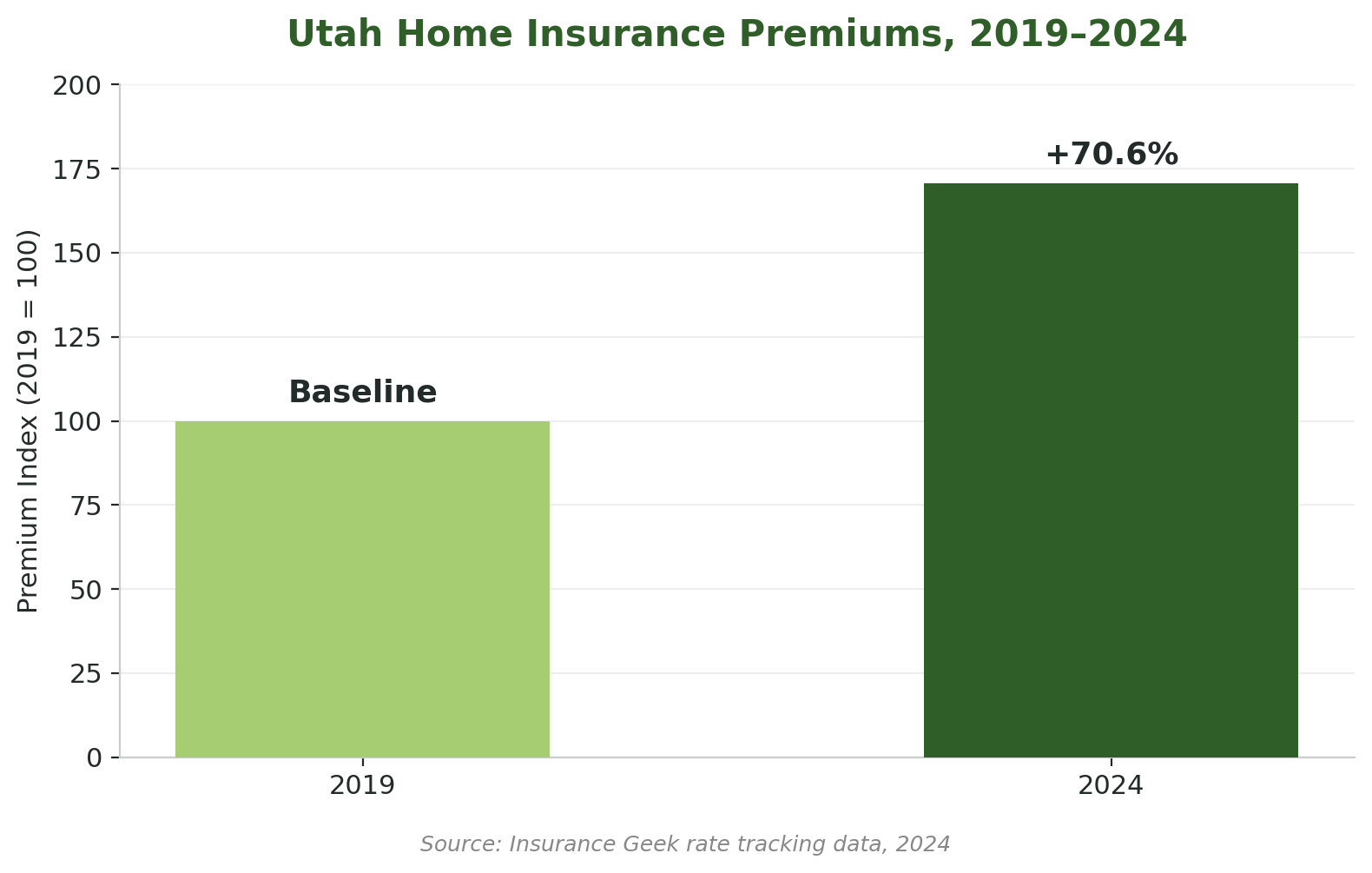

We've spent the last several years watching Utah homeowners and drivers absorb some of the steepest rate increases in the country. Utah home insurance premiums climbed a cumulative 70.6% between 2019 and 2024, according to Insurance Geek's rate tracking data, a jump second only to Colorado nationally. Auto rates followed a similar path as population growth along the Wasatch Front pushed traffic and claim frequency higher. So when industry analysts start talking about 2026 as the year things stabilize, it's worth asking what that actually means for the renewal sitting in your inbox right now.

This matters more than it sounds. A renewal increase of 8% feels manageable. A renewal increase of 30% on the same type of home, from a different carrier, means somebody left money on the table. The only way to know which one you're facing is to have someone actually compare the two.

Why Utah's Insurance Rates Climbed So Fast in the First Place

Utah's rate run wasn't random. A few things collided at once. Rebuilding costs for homes went up sharply after years of material and labor inflation. Wildfire risk maps got more aggressive, and insurers started pricing properties in the foothills and canyon communities accordingly. At the same time, more people moved to the Wasatch Front, which meant more cars on I-15 and more claims per capita.

The numbers back this up. Utah home insurance premiums rose a cumulative 70.6% from 2019 through 2024, the second-highest increase of any state behind Colorado, based on Insurance Geek's ongoing rate tracker. On the auto side, full coverage in Utah now averages around $2,565 a year, and credit score alone can shift a driver's monthly rate by roughly $155 between someone with excellent credit and someone with poor credit, according to recent industry rate analysis.

None of that is unique to one carrier. It's market-wide. That's exactly why shopping matters more now, not less.

The same pattern shows up on the auto side. Utah full coverage now averages roughly $2,565 a year, but recent 2026 rate comparisons from NerdWallet and Insurify show carriers like GEICO and Nationwide pricing full coverage for the same driver profile more than $1,000 below that average. Nobody tells you that when your renewal shows up. You only find out if someone actually checks.

What "Rates Are Stabilizing" Actually Means for Your 2026 Renewal

Industry surveys suggest more than 40% of agencies expect the hard market to ease across most lines of business in 2026. That's genuinely good news. But "the market is stabilizing" is an average, and averages hide a lot.

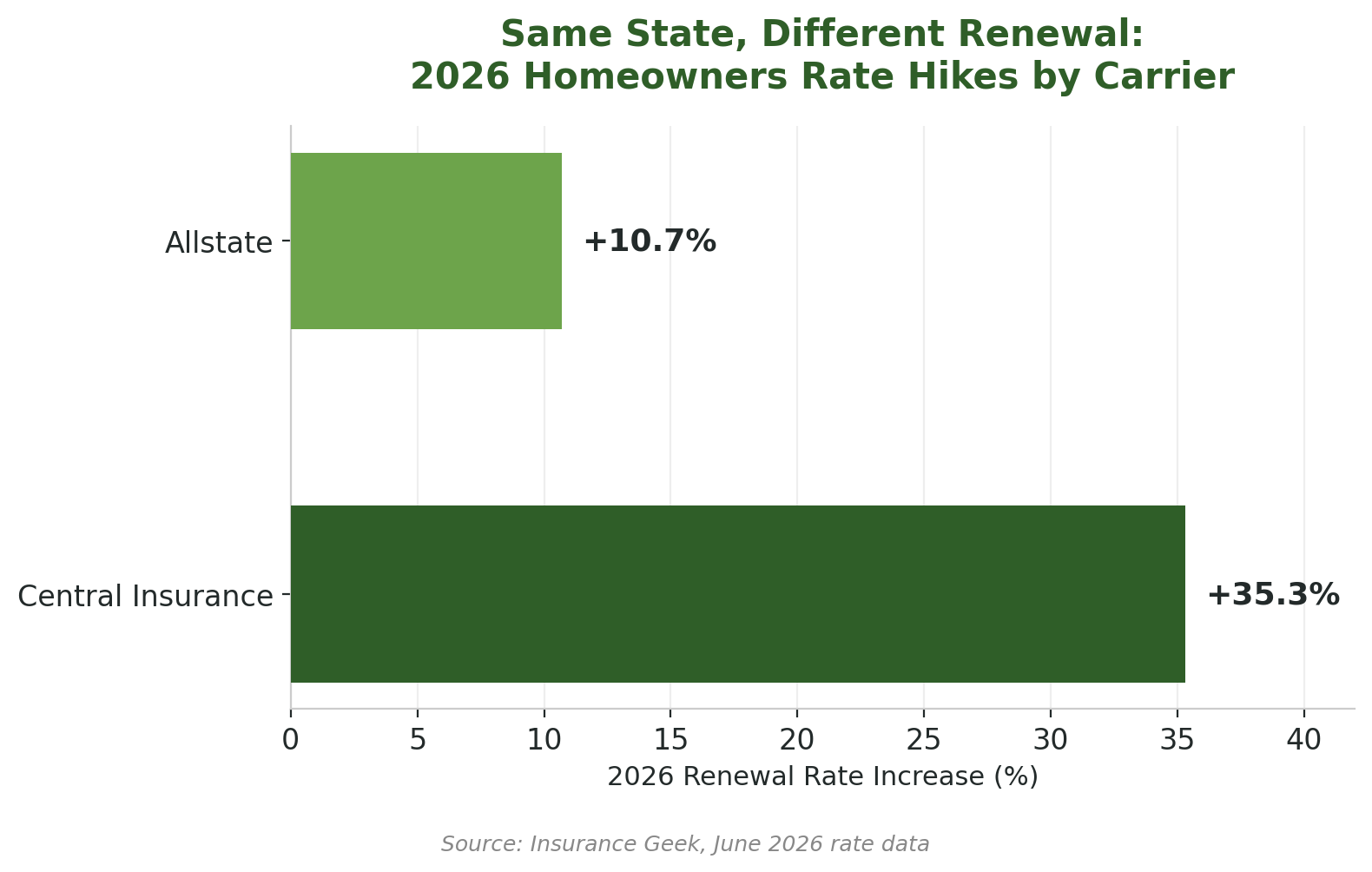

Look at what's actually happening carrier by carrier. In Utah's homeowners market this year, Openly rolled out more competitive new business pricing and capped renewal increases, while other carriers pushed rate hikes anywhere from 10.7% at Allstate to 35.3% at Central Insurance, according to Insurance Geek's June 2026 rate data. That's not a small spread. Two households with nearly identical homes could see wildly different renewal numbers depending purely on which carrier they happened to be with.

This is the part a single-carrier agent or a direct-to-consumer website can't help you with. If you're working with a captive agent, you get one company's rate, whatever it is this year. If you're comparing quotes yourself on a handful of comparison sites, you're mostly seeing marketing copy, not underwriting. An independent agent sees the actual spread across carriers and can tell you, plainly, whether your current renewal is competitive or whether it's time to move.

Why an Independent Insurance Agent in Utah Beats a Captive Agent or Comparison Site

Here's the practical difference. A captive agent, someone who works for State Farm, Allstate, or a similar single-carrier company, can only offer you that company's products. If their rates spike this year, that's the number you get. There's no alternative to shop internally.

An independent insurance agent in Utah works differently. At The Insurance Center, we work with 60-plus carriers, which means when one company has a bad underwriting year and prices up aggressively, we can place your coverage somewhere else instead of asking you to just accept the increase. We're also one of only six agencies in Utah with Big "I" Best Practices recognition, a credential that requires meeting professional standards most agencies aren't held to. That matters because it means knowing which carriers are financially stable, which ones handle claims well, and which ones are a bad fit for a given property or driving history.

Local knowledge counts here too. A national call center doesn't know that a property in Heber Valley might need different wind or snow load considerations than a similar home in Farr West. Our agents do, because we're actually here.

That local knowledge extends past homes and cars. A lot of our clients in Northern Utah also carry snowmobiles, ATVs, or boats, and those don't fit neatly into a generic online quote form. An agent who actually knows the area can tell you when a policy needs an endorsement for that equipment and when it doesn't, instead of leaving a gap you don't find out about until you're filing a claim.

A Real Example of How This Plays Out

Here's what this looked like for one Weber County client this spring. Their homeowners renewal came in with a 24% increase, driven mostly by updated wildfire risk mapping on their foothill property. Under Utah's House Bill 48, which took effect July 1, 2026, insurers now have to justify any increase over 20% if a policyholder requests it. Most people don't know that provision exists, let alone how to invoke it.

We did two things. First, we asked their current carrier to justify the increase under the new law. Second, and more importantly, we shopped the property against several other carriers who use different wildfire scoring models. The client ended up moving to a carrier with a materially better rate for the same coverage, without cutting anything from the policy. That second step, having someone who already knows which carriers price wildfire risk differently, is the part a homeowner shopping alone almost never gets access to.

We've seen a similar version of this play out on the auto side too, most often with families adding a new teen driver. A single carrier might price that addition aggressively because it doesn't want the added risk on its books. An independent agent can move just that vehicle, or the whole policy, to a carrier that prices new drivers more reasonably, without the family having to start their insurance search from scratch.

Frequently Asked Questions

Q: Is an independent insurance agent more expensive than buying insurance directly?

A: No. Carriers pay the agent's commission, so you typically pay the same premium as going direct, sometimes less since the agent can compare pricing across companies. Ask your agent to walk through this if you're unsure.

Q: What's the difference between an independent agent and a captive agent?

A: A captive agent, like one working exclusively for State Farm or Allstate, can only sell that company's products. An independent agent, like the team at The Insurance Center, represents multiple carriers and can place your coverage with whichever one fits your situation best.

Q: Will my insurance rates keep going up in Utah in 2026?

A: Probably somewhat, but less sharply than in recent years for most people. Individual carrier increases still range widely this year, from around 10% to over 35% depending on the company and property. Shopping your renewal is the only way to know where you land.

Q: Can an independent agent help if my homeowners renewal jumped more than 20%?

A: Yes. Under Utah's House Bill 48, effective July 1, 2026, insurers must justify rate increases over 20% if asked. An independent agent can request that justification and shop your policy against other carriers at the same time.

Q: How do I find out if The Insurance Center can get me a better rate?

A: Call us at (801) 622-2626. We'll compare your current policy against our network of 60-plus carriers at no cost and show you exactly where you stand.

The Bottom Line

A stabilizing market is good news, but it's an industry-wide average, not a promise about your specific renewal. The spread between carriers is still wide enough that shopping matters, maybe more than it did during the worst years of the hard market, because now there's actually room to find a better number instead of just bracing for another increase.

That's the case for working with an independent agent instead of a single carrier or a comparison website: someone needs to actually look at the spread across carriers and tell you honestly where you stand.

Ready to see whether your current renewal is actually competitive? Call The Insurance Center at (801) 622-2626, or visit us in Farr West or Heber Valley. We'll shop your policy across our carrier network and show you what's out there.

Coverage details and availability vary by policy, carrier, and state. This post is for educational purposes. Contact a licensed insurance agent at The Insurance Center for advice specific to your situation.

Contact The Insurance Center

Get A Quote

At The Insurance Center, securing your future is easy. Ready to protect what matters? Contact us for a quick quote and personalized insurance options!

Personal Insurance

From auto and homeowners to renters and umbrella policies, we help protect your family and property. Let’s find coverage that fits your life.

Commercial Insurance

We customize policies for your industry's risks, like general liability and workers' comp, ensuring you can run your business worry-free.

Recent Posts