Disability Insurance in Utah: What It Covers & Why You Need It

Your Income Is Your Biggest Asset. Are You Protecting It?

Most people insure their car, their home, and their health without a second thought. But the one thing that makes all of it possible -- your paycheck -- often goes completely unprotected. Disability insurance exists to fix that gap. If a serious illness or injury keeps you from working for months or even years, it replaces a portion of your income so you can keep the mortgage paid, the bills covered, and your family's life as stable as possible while you recover.

The odds this matters to you are higher than most people expect. According to the Social Security Administration, 1 in 4 of today's 20-year-olds will experience a disability serious enough to keep them out of work before they reach retirement age. That is not a fringe scenario. It is a quarter of the workforce.

And yet, most households are one paycheck away from financial stress. A Federal Reserve survey found that 37% of American adults could not cover a $400 emergency expense without borrowing money or selling something. Extend that to months without income and you are looking at a financial crisis that can take years to recover from. Disability insurance is the backup plan most people never think about -- until they need it.

What Is Disability Insurance?

Disability insurance replaces a portion of your income -- typically 60% to 70% -- if you are unable to work due to a covered illness or injury. That is the simple version. The coverage details matter quite a bit more than most people realize.

There are two main types: short-term and long-term. Short-term disability kicks in quickly, often within 0-14 days, and covers you for a limited period, usually 3 to 6 months. Long-term disability takes over after that and can pay benefits for years, or even through retirement age, depending on the policy terms.

The definition of 'disabled' is one of the most important things to understand in any policy. Some policies pay out if you cannot perform your own specific occupation. Others require that you cannot perform any occupation before benefits kick in. That is not a small distinction -- it is the difference between receiving a benefit check and being denied one. A licensed agent can walk you through exactly what definition applies to any policy you are considering.

Why Your Income Deserves the Same Protection as Your Home

Think about what you have already insured. You protect your car because losing it would be a financial hardship. You insure your home because replacing it would be devastating. But your income generates every other asset you are building.

Consider this: if you earn $60,000 per year and plan to work for 30 more years, your future earning potential is $1.8 million. Most households carry auto policies protecting a $30,000 vehicle but have nothing protecting the asset generating 60 times more value.

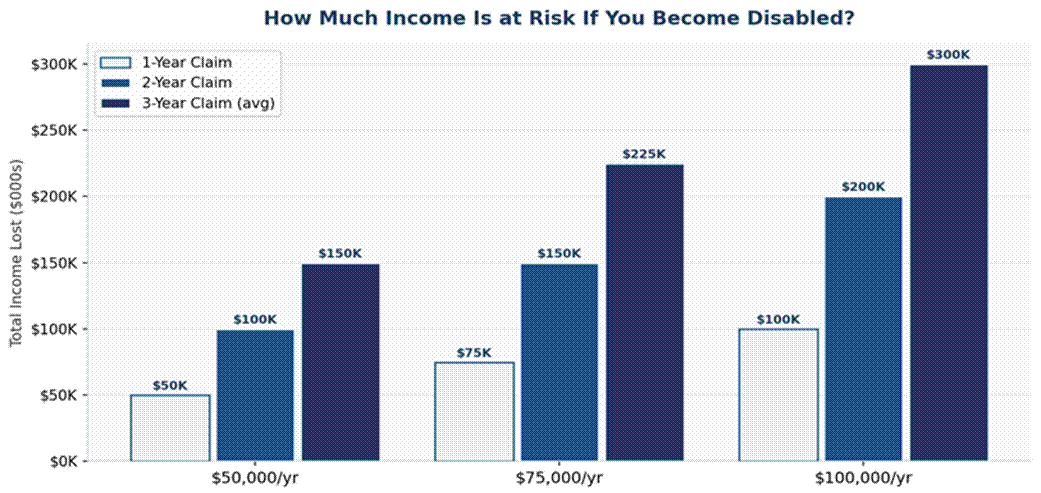

The chart below shows exactly how much income is at stake depending on your salary and how long a disability claim lasts:

Figure 1: Total income at risk by salary level and claim duration. Source: Council for Disability Awareness.

The Council for Disability Awareness reports that the average long-term disability claim lasts 34.6 months -- nearly three years. At a $60,000 annual salary, that is more than $173,000 in lost income. Long-term disability insurance would replace a significant portion of that, letting you focus on recovering instead of figuring out how to make rent.

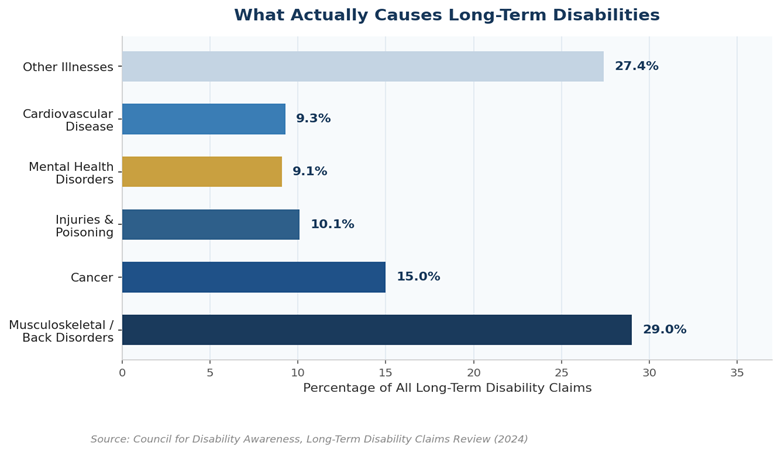

Worth mentioning here: most disabilities are not caused by dramatic workplace accidents. According to the Council for Disability Awareness, roughly 90% of long-term disability claims are triggered by illnesses, not injuries. Cancer, back disorders, heart disease, and mental health conditions are the most common culprits. You do not have to work in a dangerous profession to need this coverage.

Figure 2: Breakdown of long-term disability causes. Source: Council for Disability Awareness, Long-Term Disability Claims Review (2024).

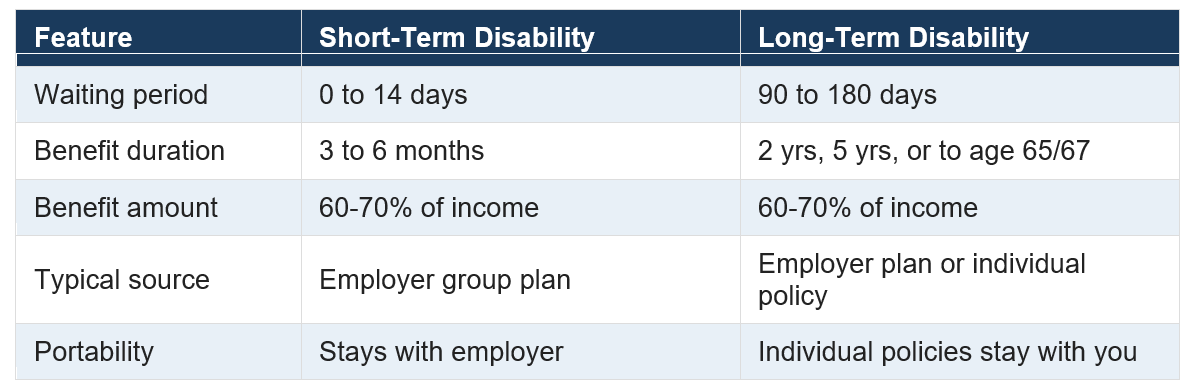

Short-Term vs. Long-Term Disability: How They Work Together

Short-term and long-term disability are designed to work together, not in isolation. Here is how they typically stack up:

The gap between where short-term coverage ends and long-term coverage begins is something to watch. If your short-term policy covers you for 3 months but your long-term policy has a 6-month waiting period, you have a 3-month window with no income replacement. Reviewing both policies together -- and identifying any gap -- is exactly the kind of thing a good independent agent catches before it becomes a problem.

Does Your Employer's Disability Coverage Actually Cover You?

Many people assume that because their employer offers disability coverage, they are fully protected. That is often not the case, for a few reasons.

Group disability policies through employers typically cover 60% of your base salary and nothing else. If you earn commissions, bonuses, or other variable compensation, that income is usually excluded. For someone in sales or any role with performance pay, that gap matters.

Group coverage also disappears when you change jobs or get laid off. If you develop a health condition while you are covered under your employer's group plan and then lose that job, finding affordable individual coverage later can be difficult. An individual disability policy you purchase on your own stays with you regardless of where you work.

There is also a tax angle most people overlook. If your employer pays your disability premiums, your benefits are taxable income when you receive them. If you pay the premiums yourself with after-tax dollars, the benefits are generally tax-free. That distinction changes what 60% of your salary actually means when you need it most.

How Much Disability Insurance Do You Actually Need in Utah?

A practical starting point is 60-70% of your gross income. The reason policies do not cover 100% is that your expenses typically decrease when you are not working -- no commuting, no work wardrobe, and potentially lower taxes. Insurers also set the cap to preserve your financial incentive to return to work.

To figure out the right number, work backwards from your fixed monthly obligations: mortgage or rent, utilities, groceries, car payments, insurance premiums, and any debt payments. That is your floor. You want your disability benefit to cover at least those costs without touching savings or going into debt.

At The Insurance Center, we help clients in Farr West and Heber Valley build coverage plans that account for what their employer already provides and fill in the gaps with an individual policy. As a Big 'I' Best Practices agency, we hold ourselves to professional standards that most independent agencies do not -- which means you are getting advice from a team that takes this seriously. And because we are independent, we shop multiple carriers to find the best fit for your situation, not the best fit for one company's product lineup.

Frequently Asked Questions About Disability Insurance

How long does it take for disability insurance benefits to start in Utah?

It depends on the policy's elimination period, which works like a time-based deductible. Short-term policies often start paying within 0-14 days. Long-term disability policies typically have elimination periods of 90-180 days, which is why pairing both types of coverage makes sense. Having solid emergency savings can also help bridge that gap.

Does disability insurance cover mental health conditions?

Most policies cover mental health conditions including depression and anxiety disorders. Some policies cap the benefit period at 24 months for mental health claims specifically. Review the policy terms carefully -- a licensed agent can show you exactly what is and is not covered before you commit.

Can I get disability insurance if I am self-employed?

Yes, and if anything it is more critical without an employer safety net. Individual disability policies are available to self-employed people. You will typically need to document your income history, but coverage is absolutely accessible regardless of employment status.

What is the difference between disability insurance and workers compensation?

Workers compensation only covers disabilities caused directly by your job or workplace. Most disabilities stem from illnesses or injuries that happen off the clock, which workers comp does not cover. Disability insurance covers you regardless of where or how the disability occurred.

How much does disability insurance cost in Utah?

Most people pay between 1% and 3% of their annual income in premiums. On a $60,000 salary, that works out to roughly $50-$150 per month. For a policy that would replace $36,000 or more per year if you could not work, that is a straightforward trade-off. Rates vary based on your age, health, occupation, and the specific terms you choose.

The Bottom Line

Your income is your most important financial asset. It funds your retirement savings, your mortgage, your kids' college account, and everything else you are building toward. For most people, it goes completely unprotected.

Disability insurance is not a product people get excited about. Neither is a smoke detector. Both exist for the moment when things go wrong, and both do their job quietly until that moment comes.

If you do not have disability coverage -- or you are not sure whether what your employer provides is enough -- now is a good time to find out. A 15-minute conversation with a licensed agent can tell you exactly where the gaps are and what it would realistically cost to close them.

Not sure if you are adequately protected? The team at The Insurance Center can review your current coverage and help you understand exactly what you have and what you might be missing. We are an independent agency, which means we work for you -- not for any one insurance company. We shop multiple carriers to find the best fit. Call us at (801) 622-2626 or stop by one of our offices in Farr West or Heber Valley to talk through your options. There is no pressure, just straight answers from people who know insurance.

By Jett Iverson, Director of Marketing | The Insurance Center Published: May 2026 | Farr West, UT, serving Northern Utah and beyond

Contact The Insurance Center

Get A Quote

At The Insurance Center, securing your future is easy. Ready to protect what matters? Contact us for a quick quote and personalized insurance options!

Personal Insurance

From auto and homeowners to renters and umbrella policies, we help protect your family and property. Let’s find coverage that fits your life.

Commercial Insurance

We customize policies for your industry's risks, like general liability and workers' comp, ensuring you can run your business worry-free.

Recent Posts